Registering a Private Limited Company in India is a strategic move for entrepreneurs looking to establish a distinct legal entity that offers numerous benefits in terms of liability protection, credibility, and growth opportunities. This guide outlines the step-by-step process of registering a Private Limited Company in India and provides a comprehensive list of essential documents required for a successful registration.

Incorporation process for Private Limited Company

Step-by-Step Registration Process:

Step 1: Obtain Digital Signature Certificates (DSC)

Step 2: Obtain Director Identification Number (DIN)

Step 3: Choose a Suitable Company Name

Step 4: Prepare and File the Incorporation Documents

Step 5: Pay the Requisite Fees

Step 6: Verification and Approval by the Registrar of Companies (ROC)

Step 7: Receive Certificate of Incorporation

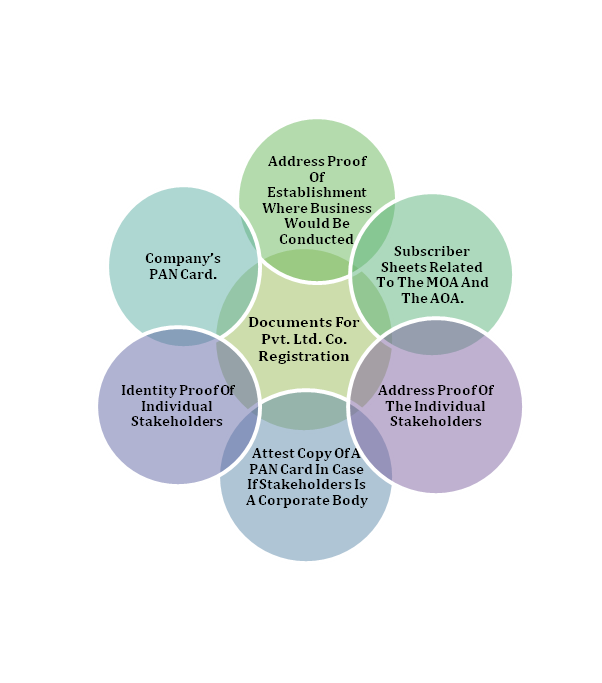

Essential Documents Required:

Memorandum of Association (e-MoA)

Articles of Association (e-AoA)

Identity and Address Proof of Directors and Shareholders

Identity Valid documents : PAN and Voter ID, DL, or Passport

Address Proof : Utility Bill, Bank statement.

Proof of Registered Office Address

Utility Bill, NOC, Rental agreement.

Declaration of Consent to Act as Director

PAN and TAN of the Jurisdictioon Details

Board Resolution for Authorizing Key Activities

Advantages of Registering as a Private Limited Company

Registering your business as a Private Limited Company in India offers a multitude of advantages that can significantly contribute to your business’s success and growth. Here are some key benefits:

Limited Liability: One of the most significant advantages of a Private Limited Company is limited liability. The liability of the shareholders is limited to their shareholding in the company. In case of financial losses or legal disputes, personal assets of shareholders are protected, providing a safety net for individual wealth.

Separate Legal Entity: A Private Limited Company is a separate legal entity distinct from its owners. This separation ensures that the company has perpetual existence, unaffected by changes in ownership or the death of shareholders.

Credibility and Trust: Being a registered legal entity, a Private Limited Company commands more credibility and trust among customers, suppliers, and partners. It enhances your company’s reputation and can attract more business opportunities.

Easy Fundraising: Private Limited Companies have better access to funding compared to other business structures. They can issue shares to raise capital from investors, venture capitalists, and even through public offerings, which can provide financial support for expansion and development.

Employee Benefits: Offering employee stock options and other benefits is easier in a Private Limited Company, making it an attractive option for hiring and retaining talented individuals.

Ownership Transfer: Shares of a Private Limited Company can be easily transferred or sold to other individuals or entities, enabling changes in ownership without disrupting the business operations.

Tax Advantages: Private Limited Companies enjoy certain tax benefits and incentives that can lower the overall tax liability. Additionally, the corporate tax rate for Private Limited Companies is generally lower than personal income tax rates.

Business Contracts: Private Limited Companies have better access to legal contracts, partnerships, and agreements, which can lead to growth opportunities and strategic collaborations.

Capacity to Sue and Be Sued: As a distinct legal entity, a Private Limited Company can sue and be sued in its own name, streamlining legal proceedings.

Professional Image: Registering as a Private Limited Company projects a professional image, which can help in attracting clients, customers, and investors.

Compliance and Regulation: Private Limited Companies are subject to regulatory oversight, which fosters transparency and accountability. This can lead to better governance and business practices.

Exit Strategy: If needed, Private Limited Companies provide a clear structure for ownership exit through share transfers or selling the business, ensuring a smooth transition.

Global Expansion: A registered Private Limited Company can engage in international business and has a better chance of establishing credibility and partnerships abroad.

Banking and Credit: Private Limited Companies have easier access to loans, credit facilities, and banking services due to their formalized structure and legal status.

Income tax audit under Section 44AB is a crucial compliance requirement, distinct from statutory audit under the Companies Act. This article provides insights into the applicability, calculation of turnover, due dates, penalties, and related aspects of income tax audit for the financial year 2022-23.

Mandatory Tax Audit:

Income tax audit applies to all companies and LLPs whose turnover or gross receipts exceed prescribed thresholds. The thresholds for other business entities and professionals are aligned with those for companies. For businesses, a turnover exceeding Rs. 10 crore triggers the audit, while for professionals, gross receipts surpassing Rs. 50 lakhs necessitate an audit.

Sr. No.

Category

Tax Audit Applicability

Conditions

1

Business

Yes

– Turnover > Rs. 10 Cr – Not opting for presumptive taxation – Cash transactions up to 5% of total gross receipts and payments

2

Business

No

Turnover < Rs. 10 Cr and Condition of 5% of Gross Receipts and Payment satisfied.

3

Business

Yes

– Turnover between Rs. 1 Cr and Rs. 10 Cr – Not opting for presumptive taxation – Cash transactions exceeding 5% of total gross receipts and payments

4

Business

No

Turnover < Rs. 2 Cr and opted for Section 44AD

5

Business

Yes

Carrying on business under specified sections with profits or gains lower than presumptive taxation limit

6

Profess.

Yes

– Turnover > Rs. 50 Lac – Not opted for presumptive taxation under 44ADA – Opted for 44ADA but claims profits below presumptive taxation limit

7

Profess.

No

Opted for presumptive taxation under 44ADA and declares profits within the prescribed limit

Calculating Turnover for Tax Audit:

For tax audit applicability, turnover is a vital parameter. In this context, turnover refers to the total sales with necessary adjustments for goods returned, price adjustments, and trade discounts, rather than just the overall sales figure. Excluded from turnover calculations are transactions involving fixed assets, rental/interest income, advances from customers, cash and trade discounts, returned goods, and sale proceeds of investments like shares and securities.

Due Date and Penalty:

The due date for tax audit of FY 2022-23 is September 30, 2023. Failure to conduct tax audit by this date attracts penalties. The penalty is either 0.5% of sales/turnover/gross receipts or Rs. 1,50,000, whichever is lower.

Limit on Chartered Accountants:

Chartered Accountants (CAs) are the only professionals authorized to sign tax audit reports. A CA can conduct a maximum of 60 tax audits, which also applies individually to each partner in a partnership firm.

Accounts Audited Under Other Laws:

If accounts are audited under other laws (e.g., statutory audit under the Companies Act), a separate audit for income tax purposes isn’t required. Only an audit report compliant with income tax regulations needs to be filed.

Tax Audit Forms:

Assessees subject to tax audit must file relevant forms along with their income tax returns. The forms include:

Form 3CA & Form 3CD: For entities audited under other laws.

Form 3CB & Form 3CD: For entities exclusively audited for income tax compliance.

Form 3CE: For non-residents and foreign companies receiving royalty/fees for technical services.

Tax Audit Report Revision and Penalty Waiver:

Tax audit reports can be revised multiple times through the income tax portal. Penalty waivers are possible if reasonable causes are provided for non-submission of tax audit reports by the deadline.

In conclusion, understanding income tax audit under Section 44AB is vital for businesses and professionals to ensure compliance with the law and avoid penalties.

Disclaimer:

The information provided in the above article is intended for general informational purposes only and should not be construed as professional advice. The article is based on the latest amendment applicable to FY 2022-23 and is subject to change based on updates to tax laws, regulations, and guidelines. Readers are advised to consult with qualified tax professionals, accountants, or legal advisors to obtain accurate and up-to-date information specific to their individual circumstances. While every effort has been made to ensure the accuracy of the information presented, no responsibility or liability is assumed for any errors or omissions in the content. Tax regulations and laws can be complex and subject to interpretation, and the application of these rules may vary based on individual circumstances. The author and publisher of this article disclaim any liability for actions taken or decisions made based on the information provided herein. Readers are encouraged to independently verify the accuracy and applicability of the information provided before making any financial or legal decisions.

ln order to address these issues, a Press Release dated 28.6.2023 (copy enclosed) was issued by Ministry of Finance wherein the following decisions relating to income-tax have been taken:

first Rs 7 lakh remittance under LRS there shall be no TCS. Beyond this Rs 7 lakh threshold, TCS shall be at the rate of –

0.5% (if remittance for education is financed by loan taken from a financial institution);

5% (in case of remittance for education/medical treatment);

20% for others.

For purchase of overseas tour program package under clause (ii) of sub-section (1G) of section 206C, the TCS shall continue to apply at the rate of 5% for the first Rs 7 lakh per individual per annum, and the 20% rate will only apply for expenditure above this limit

lncreased TCS rates to applicable from 1st October, 2023:

The increase in TCS rates; which were to come into effect from 1’t July,2023 shall now come into effect from 1″t October, 2023 with the modification as in (i) above. Till 30th September, 2023, earlier rates (prior to amendment by the Finance Act, 2023) shall continue to apply.

Earlier and new TCS rates are summarised as under:

Nature of payment (1)

Earlier rate before Finance Act,2023 (2)

New rate w.e.f 1st October, 2023 (3)

LRS for education, financed by loan from financial institution

Nil upto Rs 7 lakh 0.5% above Rs T lakh

Nil upto Rs 7 lakh 0.5% above Rs 7 lakh

LRS for Medical treatment/ education (other than financed by loan)

Nil upto Rs 7 lakh 5% above Rs 7 lakh

Nil upto Rs 7 lakh 5% above Rs 7 lakh

LRS for other purposes

Nil upto Rs 7 lakh 5% above Rs 7 lakh

Nil upto Rs 7 lakh 20% above Rs 7 lakh

Purchase of Overseas tour program package

5% (without threshold)

5% till Rs 7 lakh, 20% thereafter

*Note:

(i) TCS rate mentioned in column 2 shall continue to apply till 30” September,2023.

(ii) There shall be no TCS on expenditure under LRS under clause (i) of subsection (1G) of section 206C upto Rs 7 lakh, irrespective of purpose.

Sub-section (1-l) of section 206C of the Act provides that if any difficulty arises in giving effect to the provisions of sub-section (1G) of this section, the Board may, with the approval of the Central Government, issue guidelines for the purpose of removing the difficulty. Accordingly, the following guideline is issued under this provision.

FAQ:-

Question 1:

Whether payment through overseas credit card would be counted in LRS?

Answer: As announced in the press release dated 28th June, 2023, the classification of use of international credit card while being overseas, as LRS is postponed. Therefore, no TCS shall be applicable on expenditure through international credit card while being overseas till further order.

Question 2:

Whether the threshold of Rs 7 lakh, for TCS to become applicable on LRS, applies separately for various purposes like education, health treatment and others? For example, if remittance of Rs 7 lakh under LRS is made in a financial year for education purpose and other remittances in the same financial year of Rs 7 lakh is made for medical treatment and Rs 7 lakh for other purposes, whether the exemption limit of Rs 7 lakh shall be given to each of the three separately?

Answer: lt is clarified that the threshold of Rs 7 lakh for LRS is combined threshold for applicability of the TCS on LRS irrespective of the purpose of the remittance. This is clear from the first proviso to sub-section (1G) of section 206C of the Act. The proviso states that the TCS is not required if the amount or aggregate of the amounts being remitted by a buyer is less than seven Iakh rupees in a financial year. The amendment by the Finance Act, 2023 has only restricted it to education and medical treatment purpose. Now, after press release, old position has been restored and the threshold continues to apply for seven lakh rupees in a financial year, irrespective of the purpose.

Thus, in the given example, upto Rs 7 lakh remittance under LRS during a financial year shall not be liable for TCS. However, subsequent Rs 14 lakh remittance under LRS shall be liable for TCS in accordance with the TCS rates applicable for such remittance.

ln the example, if the remittances under LRS are made in the current financial year at different point of time, TCS rates for the remaining Rs 14 lakh remittances under LRS would depend on the time of remittance as TCS rates changes from 1st October 2023.

TCS rates would be applicable as under:-

First Rs 7 lakh remittance under LRS during the financial year 2023-24 for education purpose (or for that matter any purpose)

No TCS

Remittances beyond Rs 7 lakh under LRS during the financial year 2023-24, if on or before 30th September 2023

TCS 5% (irrespective of the purpose unless it is for education purpose financed by loan from a financial institution when the rate is 0.5%)

Remittances beyond Rs 7 lakh under LRS during the financial year 2023-24, if on or after 1’t October 2023

TCS at O.5o/o (if it is for education purpose financed by loan from a financial institution), 5% (if it is for education or medical treatment) and 20% (if it is for other purposes)

Question 3: Since there are different TCS rates on LRS for the first six months and next six months of the financial year 2023-24, whether the threshold of Rs 7 lakh, for the TCS to become applicable on LRS, applies separately for each six months?

Answer: No. The threshold of Rs 7 lakh, for the TCS to become applicable on LRS, applies for the full financial year. lf this threshold has already been exhausted; all subsequent remittances under LRS, whether in the first half or in the second half, would be liable for TCS at applicable rate.

Question 4: Whether the threshold of Rs 7 lakh, for TCS to become applicable on LRS, applies separately for each remittance through different authorised dealers? lf not, how will authorised dealer know about the earlier remittances by that remitter through some other authorised dealer?

Answer: lt is clarified that the threshold of Rs 7 lakh for LRS is qua remitter and not qua authorised dealer. This is clear from the first proviso to sub-section (1G) of section 206C of the Act. The proviso states that the TCS is not required if the amount or aggregate of amounts being remitted by a buyer is less than seven lakh rupees in a financial year. The threshold continues to apply qua remitter.

Since the facility to provide real time update of remittance under LRS by remitter is still under development by the RBl, it is clarified that the details of earlier remittances under LRS by the remitter during the financial year may be taken by the authorised dealer through an undertaking at the time of remittance. lf the authorised dealer correctly collects the tax at source based on information given in this undertaking, he will not be treated as “assessee in default”. However, for any false information in the undertaking, appropriate action may be taken against the remitter under the Act.

It is further clarified that same methodology of taking undertaking from the buyer of overseas tour program package may be followed by the seller of such package.

Question 5: There is threshold of Rs 7 lakh for remittance under LRS for TCS to become applicable while there is another threshold of Rs 7 lakh for purchase of overseas tour program package where reduced rate of 5% TGS applies. Whether these two thresholds apply independently?

Answer: Yes, these two thresholds apply independently. For LRS, the threshold of Rs 7 lakh applies to make TCS applicable. For purchase of overseas tour program package, the threshold of Rs 7 lakh applies to determine the applicable TCS rate as 5% or 20%

Question 6: A resident individual spends Rs 3 lakh for purchase of overseas tour program package from a foreign tour operator and remits money which is classified under LRS. There is no other remittance under LRS or purchase of overseas tour program during the financial year. Whether TCS is applicable?

Answer: ln case of purchase of overseas tour program package which is classified under LRS, TCS provision for purchase of overseas tour program package shall apply and not TCS provisions for remittance under LRS.

Since for purchase of overseas tour program package, the threshold of Rs 7 lakh for applicability of TCS does not apply, TCS is applicable and tax is required to be collected by the seller. ln this case the tax shall be required to be collected at 5o/o since the total amount spent on purchase of overseas tour program package during the financial year is less than Rs 7 lakh. The TCS should be made by the seller.

Question 7: There are different rates for remittance under LRS for medical treatment/education purposes and for other purposes. What is the scope of remittance under LRS for medical treatment/education purposes?

Answer: As per the clarification by the RBl, remittance for the purposes of medical treatment shall include,-

remittance for purchase of tickets of the person to be treated medically overseas (and his attendant) for commuting between lndia and the overseas destination;

his medical expense; and

other day to day expenses required for such purpose.

It may be noted that code 50304 (under the Purpose Group Name “Travel”), in RBI master direction for LRS, pertains to travel for medical treatment. As per BPM6, A.P. (DlR Series) Circular no 50, dated 11 Feb 2016 this code covers the transactions which are related to health services acquired by residents travelling abroad for medical reasons, which includes medical services, other healthcare, food, accommodation and local transport transactions

ln addition, code 51108 (under the Purpose Group Name “Personal, Cultural & Recreational services”) covers transactions for health services rendered remotely or onsite (that is no travel by service recipient is involved). This cover services from hospitals, doctors, nurses, paramedical and similar services, etc. TCS provision for purpose of medical treatment would apply when remittance is under code 50304 or under code 51 108.

Education :

Remittance for purpose of education shall include,-

remittance for purchase of tickets of the person undertaking study overseas for commuting between lndia and the overseas destination;

the tuition and other fees to be paid to educational institute; and

other day to day expenses required for undertaking such study

It may be noted that code 50305 (under the Purpose Group Name “Travel”), in RBI master direction for LRS, pertains to travel for education (including fees, hostel expenses, etc). As per BPM6, A.P. (DIR Series) Circular no 50, dated 11 Feb 2016 this code covers education related services such as tuition, food, accommodation, local transport and health services acquired by resident students while residing overseas. tn addition, code 51107 (under the Purpose Group Name “Personal, Cultural & Recreational services”) covers transactions for education (eg fees for correspondence courses abroad) where the person receiving education does not travel overseas. TCS provision for purpose of education would apply when remittance is under code 50305 or under 51 1 07.

Question 8: Whether purchase of international travel ticket or hotel accommodation on standalone basis is purchase of overseas tour program package?

Answer: The term ‘overseas tour program package’ is defined as to mean any tour package which offers visit to a country or countries or territory or territories outside lndia and includes expenses for travel or hotel stay or boarding or lodging or any other expenditure of similar nature or in relation thereto.

It is clarified that purchase of only international travel ticket or purchase of only hotel accommodation, by in itself is not covered within the definition of ‘overseas tour program package’. To qualify as ‘overseas tour program package’, the package should include at least two of the followings:-

international travel ticket,

hotel accommodation (with or without food)/boarding/lodging,

any other expenditure of similar nature or in relation thereto.

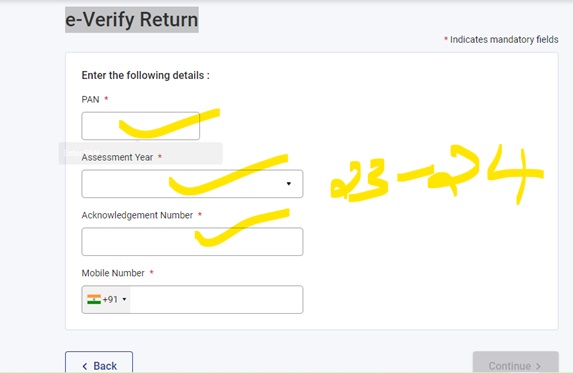

CHOOSE THE RIGHT ITR FORMS WHILE FILING THE RETURN

Income tax filing can be a daunting task for many individuals. With changing regulations and evolving tax laws, it’s essential to stay updated on the latest requirements to ensure accurate and timely filing. In this blog post, we will discuss the income tax filing forms to be used for the Assessment Year (AY) 2023-24, covering the Financial Year (FY) 2022-23. By understanding the purpose and significance of these forms, you’ll be better equipped to navigate the process with confidence.

Form ITR-1, also known as SAHAJ, is primarily designed for individuals having income from salary, one house property, or other sources like interest. It is one of the most commonly used forms by salaried individuals or pensioners who have a straightforward income structure. ( For individuals being a resident (other than not ordinarily resident) having total income upto Rs.50 lakh, having Income from Salaries, one house property, other sources (Interest etc.), and agricultural income upto Rs.5 thousand.

Form ITR-2 is applicable for individuals and Hindu Undivided Families (HUFs) not eligible to file Form ITR-1. It includes individuals with income from multiple sources, such as salary, house property, capital gains, and more. If you have earned income from foreign assets, or you are a director in a company, or have invested in unlisted equity shares, this form is suitable for you. (For Individuals and HUFs not having income from profits and gains of business or profession)

Form ITR-3 is specifically meant for individuals and HUFs having income from business or profession. If you are a self-employed professional or a partner in a partnership firm, this form is suitable for reporting your income, deductions, and business-related details.(For individuals and HUFs having income from profits and gains of business or profession.)

Form ITR-4, also known as SUGAM, is applicable for individuals, HUFs, and firms (other than LLPs) having a presumptive income from business or profession. This form simplifies the process for small taxpayers who opt for the presumptive taxation scheme under Section 44AD, 44ADA or 44AE and agricultural income upto Rs.5 thousand.)

Form ITR-5 is for individuals, HUFs, firms, Association of Persons (AOPs), and Body of Individuals (BOIs) who are not eligible to file forms ITR-1 to ITR-4. It is suitable for reporting income from partnership firms, LLPs, or income from multiple sources for which other forms are not applicable. (For persons other than- (i) individual, (ii) HUF, (iii) company and (iv) person filing Form ITR-7

Form ITR-6 is specifically designed for companies, excluding those claiming exemption under Section 11 (Income from property held for charitable or religious purposes).

Form ITR-7 is for individuals, companies, and entities that are required to furnish a return under Section 139(4A), Section 139(4B), Section 139(4C), or Section 139(4D) of the Income Tax Act. This form is applicable for reporting income of trusts, political parties, institutions, and more.

Choosing the right income tax filing form is crucial to ensure accurate reporting of income and compliance with tax regulations. By understanding the purpose and applicability of each form, individuals can effectively file their returns for the Assessment Year 2023-24, covering the Financial Year 2022-23. Stay informed, seek professional assistance if needed, and fulfill your tax obligations seamlessly.

Contact a Professional for Error-Free Income Tax Returns

a comprehensive understanding of advance tax in India,

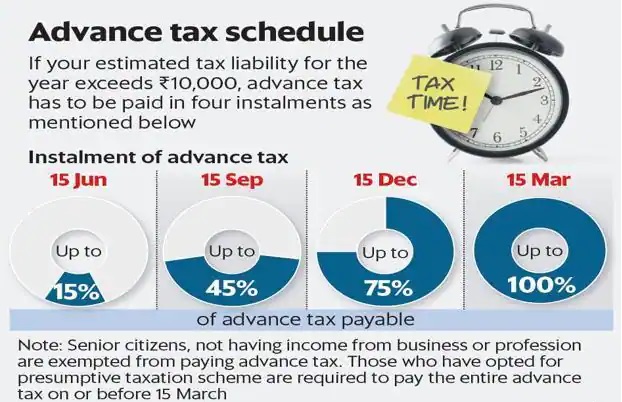

Advance tax in India is a system under which taxpayers are required to pay a portion of their tax liability in advance, throughout the financial year, rather than paying the entire tax liability at the end of the year. The purpose of this system is to ensure that taxpayers have sufficient funds to pay their tax liability when it becomes due.

In India, advance tax is applicable to individuals, HUFs, firms and companies. The advance tax liability is calculated based on the estimated tax liability for the financial year. Taxpayers are required to pay advance tax in instalments, as per the following schedule:

15% of advance tax liability on or before 15th June of the financial year

45% of advance tax liability on or before 15th September of the financial year

75% of advance tax liability on or before 15th December of the financial year

100% of advance tax liability on or before 15th March of the financial year

If a taxpayer fails to pay the advance tax as per the above schedule, they may be subject to interest under section 234B and 234C of the Income Tax Act.

It’s important to note that the rules and regulations regarding Advance tax in India may change from time to time, and it is recommended to consult with a Chartered Accountant or Tax professional for the most accurate and up-to-date information.

In case of non-compliance of advance tax in India, the taxpayer may be subject to interest under section 234B and 234C of the Income Tax Act.

Under Section 234B, if a taxpayer fails to pay the advance tax as per the due dates specified, they will be charged interest at the rate of 1% per month on the unpaid amount of advance tax.

Under Section 234C, if a taxpayer fails to pay the advance tax as per the due dates specified, they will be charged interest at the rate of 1.5% per month on the unpaid amount of advance tax.

It’s important to note that if the taxpayer can prove that there was reasonable cause for not paying the advance tax on time, the interest may be waived by the tax authorities.

It’s important to note that the rules and regulations regarding interest for non-compliance of advance tax in India may change from time to time, and it is recommended to consult before paying with tax professionals like us. It’s always important to comply with the tax laws to avoid any penalties or interest.

Navigating the world of estate planning can often feel like wandering through a complex maze, filled with unfamiliar terminology and intricate strategies. I, like many advisors, faced these challenges when I first began my journey. I encountered obstacles, made errors, and gained valuable lessons along the way.

Today, I am thrilled to share three simple yet impactful tips that I wish I had known from the start. Let’s delve into them:

Tip #1: Prioritize Liquidity and Income Accumulation During the early stages of my career, I often emphasized asset accumulation to my clients. However, I later discovered that insurance products primarily aim to create liquidity. This realization struck me: as advisors, we should encourage our clients to focus on income accumulation and liquidity. Why? Because assets such as property can become burdensome, particularly in old age. The true objective of estate planning is to ensure a steady income for your clients.

Tip #2: Identify Risks Within the Estate Consider the potential risks that could affect the estate. Could illness strike? What happens if retirement arrives without a reliable income? Will the children require funds for their education? Identifying these risks allows you to demonstrate to your clients how financial products can provide coverage during unforeseen circumstances.

Tip #3: Recognize Multiple Generations Within a Family With the prolonging of life expectancy, multiple generations often coexist within a single family. This dynamic presents unique challenges, especially regarding the equitable distribution of inheritance. Effective estate planning can establish a harmonious balance among all family members, mitigating the potential for conflicts.

Now, I want to emphasize an element that is frequently underestimated in estate planning: insurance. It extends far beyond being a mere safety net. When strategically integrated into an estate plan, insurance becomes a powerful tool for income accumulation, tax planning, and the creation of liquidity.

Insurance serves as a shield against unexpected life events, and it can even function as a financial asset in itself. Moreover, it acts as a catalyst for seamless wealth transfer. As we navigate the complexities of estate planning, let us not overlook the versatility of insurance and its capacity to enhance the impact of our strategies.

By keeping these tips in mind, my advisory practice underwent a transformative shift, and I am confident that they can yield similar results for you. These insights will empower you to provide your clients with the most effective and personalized advice possible.

Are you ready to delve deeper into estate planning and explore additional strategies? Secure your lifetime access to the three-hour estate planning for advisors course here: https://chat.whatsapp.com/9qndS5YIuq5GumkJHfvC7K. It’s an opportunity to expand your knowledge and refine your expertise in estate planning.

MONDAY TO FRIDAY

ZOOM MEETING ID GROUPMeeting ID: 797 9296 0478 Passcode: xxxxxx JOINT WHATSAPP GROUP TO VIEW PASS CODE.

Cryptocurrencies have gained significant popularity in recent years, and their taxability has become a topic of interest, especially in India. While the Indian government did not have an official stance on the categorization and taxation of crypto assets until 2022, the landscape has changed. In this article, we will explore the current tax regulations surrounding cryptocurrencies in India and shed light on key considerations for taxpayers.

Taxes on Cryptocurrency in 2023:

When it comes to cryptocurrency trading, selling, or spending earnings in India, a 30% tax is applicable. Additionally, a 1% Tax Deducted at Source (TDS) is imposed on sales of cryptocurrency assets exceeding ₹50,000 in a single fiscal year. Individuals engaged in other forms of cryptocurrency income, such as mining or staking, may also be subject to income tax at their individual tax rates upon receipt.

How Cryptocurrency is Taxed in India:

Under Section 2(47A) of the Income Tax Act, cryptocurrencies are classified as “Virtual Digital Assets” (VDAs). This definition encompasses various crypto assets, including cryptocurrencies, NFTs, tokens, and more. The 2022 budget introduced Section 115BBH, imposing a 30% tax (plus surcharge and cess) on gains from cryptocurrency trading starting from April 1, 2022. This tax rate is equivalent to the highest income tax band in India, irrespective of the type of income or its duration. Furthermore, a 1% TDS is applicable on the transfer of cryptocurrency assets from July 1, 2022, if the transactions exceed ₹50,000 in a financial year (or ₹10,000 in specific cases).

Key Points to Note about Crypto Tax in India:

Cryptocurrency asset profits are subject to a 30% tax rate (plus surcharge and cess).

Section 115BBH of the tax code governs cryptocurrency profits.

No option for a lower long-term capital gains tax rate is available.

Deductions other than purchase costs are not permitted.

A 1% TDS is levied on the transfer of VDAs.

The 30% tax rate is effective from April 1, 2022, and the 1% TDS rate from July 1, 2022.

When are Taxes Due on Cryptocurrencies in India?

You may be liable to pay the 30% tax rate whenever you engage in the following transactions:

Purchasing cryptocurrency using Indian rupees or any other fiat currency.

Trading stable coins and other cryptocurrencies.

Using cryptocurrency to make purchases.

However, there are instances where the 30% tax rate may not be applicable. In such cases, tax will be due upon receipt at your individual tax rate. Examples include:

Receiving cryptocurrency as a gift (refer to gift section for details).

Coin mining (refer to mining section for details).

Using cryptocurrency for payments.

Earning stake benefits.

Receiving airdrops.

TDS on Crypto Assets:

A 1% TDS is charged on the transfer of crypto assets. TDS is collected at the time of the transaction or source. The primary purpose of this 1% TDS is to ensure transaction reporting and track investments made by Indian investors in cryptocurrency. It is important to note that a transfer refers to a change of ownership, such as a sale, exchange, or expenditure, and not merely transferring funds between wallets.

Set Off of Losses

Losses from cryptocurrency investments cannot be offset against cryptocurrency profits or any other gains or income, as per Section 115BBH. Furthermore, apart from the acquisition cost or purchase price, no deductions other than purchase costs are allowed for cryptocurrency investors

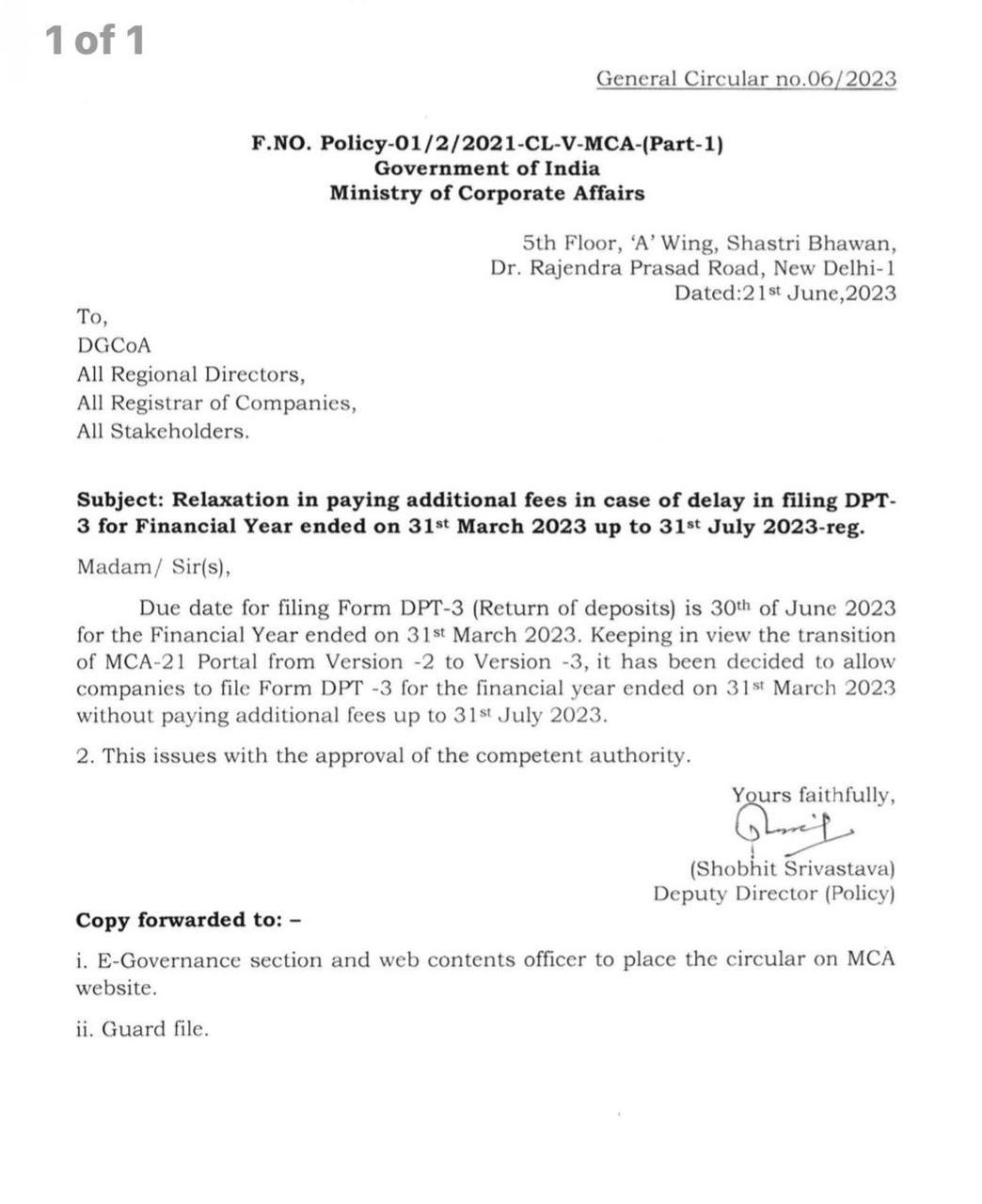

The announcement was made through General Circular no. 06/2023 issued by the Ministry. The extension in the due date provides relief to companies, allowing them more time to comply with the filing requirements for the Financial Year ended on March 31, 2023. By extending the deadline, companies can avoid paying additional fees that would have been applicable for late filing. This decision acknowledges the challenges posed by the transition of the MCA-21 Portal and aims to facilitate a smoother filing process for businesses.

Now for the Financial Year 2022-23 Extended-

Due date for filing Form DPT-3 (Return of deposits) is 30th of June 2023 for the Financial Year ended on 31st March 2023. Keeping in view the transition of MCA-21 Portal from Version-2 to Version-3, it has been decided to allow companies to file Form DPT-3 for the financial year ended on 31st March 2023 without paying additional fees up to 31st July 2023.

Taxation is an essential component of any country’s economic system, providing the necessary revenue for the government to fund public services and infrastructure. In India, where the small business sector plays a significant role in driving economic growth and employment, the concept of presumptive taxation has emerged as a simplified tax regime. Designed specifically for small businesses, this system aims to reduce the compliance burden and promote ease of doing business. In this article, we will explore the concept of presumptive taxation in India and its benefits for small business owners.

Presumptive taxation is a method of calculating and paying taxes based on a presumed income or profit percentage. It offers an alternative to the traditional system of maintaining meticulous accounting records and undergoing complex tax assessments. Introduced under Section 44AD, 44ADA, and 44AE of the Income Tax Act, 1961, presumptive taxation primarily targets small businesses and professionals with a turnover below a specified threshold.

Eligible businesses include individuals, Hindu Undivided Families (HUFs), and partnerships with a total turnover or gross receipts of up to Rs. 2 crore in a financial year. These businesses can opt for the presumptive taxation scheme and declare their income as a percentage of total turnover, thereby avoiding the need for detailed bookkeeping.

Professionals such as doctors, lawyers, engineers, architects, accountants, and other specified professionals can avail of the presumptive taxation scheme under Section 44ADA. They can declare 50% of their gross receipts as their taxable income, eliminating the requirement for maintaining books of accounts. Gross Turnover upto Rs. 50 Lakhs and From FY 2023-24 Rs.75 Lakhs Per Annam.

Section 44AE is applicable to owners of goods carriage vehicles who can determine their income based on the number of vehicles owned and utilized for business purposes. A fixed presumptive income per vehicle is calculated, taking into account the load capacity and distance covered, thereby simplifying the tax calculation process. applicable for upto 10 Vehicles Owned Per year

Benefits of Presumptive Taxation

Reduced Compliance Burden: Presumptive taxation significantly reduces the compliance burden for small businesses and professionals. By eliminating the need for maintaining detailed accounting records and undergoing extensive tax assessments, this system saves valuable time and resources.

Simplified Tax Calculation: Under the presumptive taxation scheme, taxpayers can determine their taxable income based on a predetermined percentage of their total turnover or gross receipts. This simplicity makes tax calculation more straightforward and less prone to errors.

Presumptive Income Benefits: The presumed income percentage set by the government is generally lower than the actual profit margins earned by small businesses and professionals. This implies that taxpayers can enjoy the advantage of a lower tax liability, enhancing their overall profitability.

Cash Flow Management: By opting for presumptive taxation, small businesses can manage their cash flow effectively. The tax liability is calculated based on turnover, eliminating the need to wait for actual realization of payments before paying taxes.

Increased Taxpayer Base: Presumptive taxation has encouraged more small businesses and professionals to enter the formal tax system. The simplified compliance requirements make it easier for previously unregistered entities to join the mainstream economy, fostering transparency and accountability.

NEED SUNMARG HELP?

Prefer speaking with a human to file your Return for FY 2022-23?. Schedule a Call and File Return with us or Visit our office for Live Filing

{kind=link}