Registering a Private Limited Company in India

Registering a Private Limited Company in India is a strategic move for entrepreneurs looking to establish a distinct legal entity that offers numerous benefits in terms of liability protection, credibility, and growth opportunities. This guide outlines the step-by-step process of registering a Private Limited Company in India and provides a comprehensive list of essential documents required for a successful registration.

Incorporation process for Private Limited Company

Step-by-Step Registration Process:

- Step 1: Obtain Digital Signature Certificates (DSC)

- Step 2: Obtain Director Identification Number (DIN)

- Step 3: Choose a Suitable Company Name

- Step 4: Prepare and File the Incorporation Documents

- Step 5: Pay the Requisite Fees

- Step 6: Verification and Approval by the Registrar of Companies (ROC)

- Step 7: Receive Certificate of Incorporation

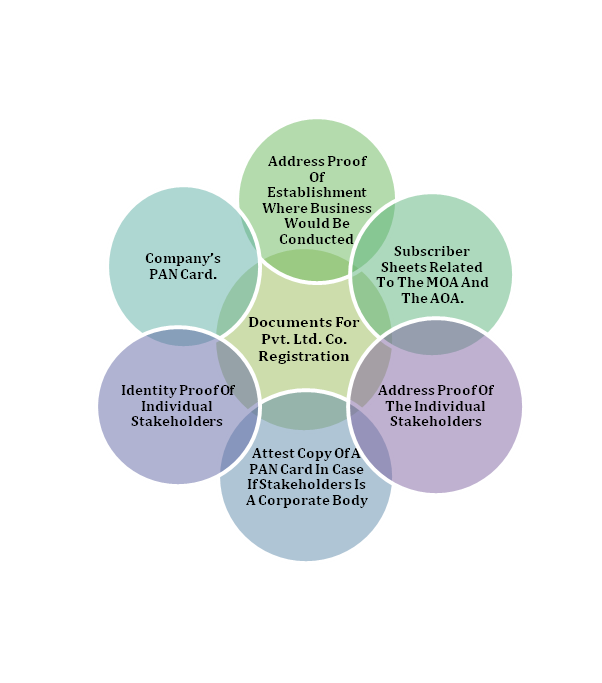

Essential Documents Required:

- Memorandum of Association (e-MoA)

- Articles of Association (e-AoA)

- Identity and Address Proof of Directors and Shareholders

Identity Valid documents : PAN and Voter ID, DL, or Passport

Address Proof : Utility Bill, Bank statement.

- Proof of Registered Office Address

Utility Bill, NOC, Rental agreement.

- Declaration of Consent to Act as Director

- PAN and TAN of the Jurisdictioon Details

- Board Resolution for Authorizing Key Activities

Advantages of Registering as a Private Limited Company

Registering your business as a Private Limited Company in India offers a multitude of advantages that can significantly contribute to your business’s success and growth. Here are some key benefits:

- Limited Liability: One of the most significant advantages of a Private Limited Company is limited liability. The liability of the shareholders is limited to their shareholding in the company. In case of financial losses or legal disputes, personal assets of shareholders are protected, providing a safety net for individual wealth.

- Separate Legal Entity: A Private Limited Company is a separate legal entity distinct from its owners. This separation ensures that the company has perpetual existence, unaffected by changes in ownership or the death of shareholders.

- Credibility and Trust: Being a registered legal entity, a Private Limited Company commands more credibility and trust among customers, suppliers, and partners. It enhances your company’s reputation and can attract more business opportunities.

- Easy Fundraising: Private Limited Companies have better access to funding compared to other business structures. They can issue shares to raise capital from investors, venture capitalists, and even through public offerings, which can provide financial support for expansion and development.

- Employee Benefits: Offering employee stock options and other benefits is easier in a Private Limited Company, making it an attractive option for hiring and retaining talented individuals.

- Ownership Transfer: Shares of a Private Limited Company can be easily transferred or sold to other individuals or entities, enabling changes in ownership without disrupting the business operations.

- Tax Advantages: Private Limited Companies enjoy certain tax benefits and incentives that can lower the overall tax liability. Additionally, the corporate tax rate for Private Limited Companies is generally lower than personal income tax rates.

- Business Contracts: Private Limited Companies have better access to legal contracts, partnerships, and agreements, which can lead to growth opportunities and strategic collaborations.

- Capacity to Sue and Be Sued: As a distinct legal entity, a Private Limited Company can sue and be sued in its own name, streamlining legal proceedings.

- Professional Image: Registering as a Private Limited Company projects a professional image, which can help in attracting clients, customers, and investors.

- Compliance and Regulation: Private Limited Companies are subject to regulatory oversight, which fosters transparency and accountability. This can lead to better governance and business practices.

- Exit Strategy: If needed, Private Limited Companies provide a clear structure for ownership exit through share transfers or selling the business, ensuring a smooth transition.

- Global Expansion: A registered Private Limited Company can engage in international business and has a better chance of establishing credibility and partnerships abroad.

- Banking and Credit: Private Limited Companies have easier access to loans, credit facilities, and banking services due to their formalized structure and legal status.